A budget might sound boring, but it really does make life easier. Setting some boundaries around your spending can help you avoid that “Where did my money go?” moment and feel more in control of your money.

This guide walks you through the basics of building a simple, realistic budget. It can help you spot what’s working, where something might need adjusting, and when it might be time to call in some extra support.

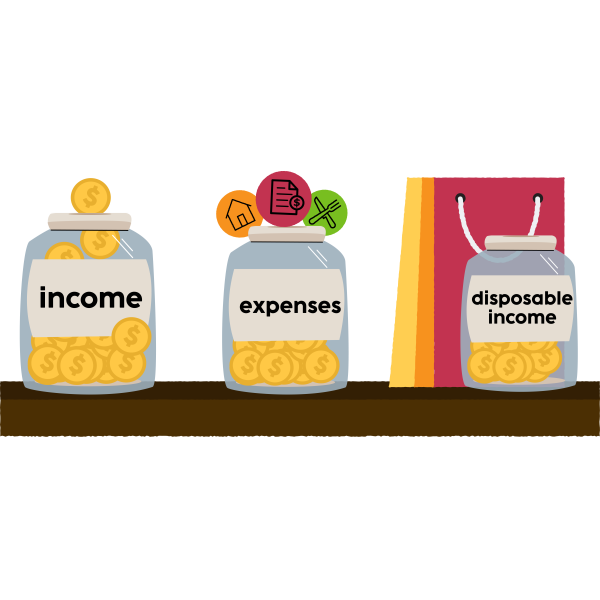

money in, money out

Think of a budget as a snapshot of your money. It shows what money is coming in, what you spend, and what’s left over. Your budget can be as simple or as detailed as you like, but generally includes three main parts:

This is any money you receive on a regular basis, like:

- wages or salary

- Centrelink or other support payments

- irregular income from side gigs, casual work, gifts etc

- money from family

- interest from savings.

This is everything you spend your money on. It can help to group these into categories like:

Essentials - things you rely on for everyday living, study or work

- rent, board or mortgage payments

- electricity, water and gas bills

- phone and internet bills

- groceries and cleaning supplies

- transport (e.g. public transport, car registration, parking and fuel)

- medication or health costs

- insurance (e.g. health, car, home or rental insurance)

- basic clothing and toiletries

- childcare or school costs.

Other regular commitments – other reoccurring payments, like:

- streaming subscriptions

- debt payments (loans, credit cards etc)

- gym or club memberships

- family support (e.g. shared expenses, sending money to relatives)

- charity or donations (e.g. faith-based obligations, classes, fundraising).

Unexpected expenses – costs that can pop up from time to time, like:

- repairs

- extra medical costs

- unexpected travel

- replacing broken items

- gifts

- pet costs

- cultural obligations (e.g. events, ceremonies).

This is what's left over. You can choose to save it, put some aside for future costs or spend it on things like:

- eating out and socialising

- entertainment

- activities and hobbies.

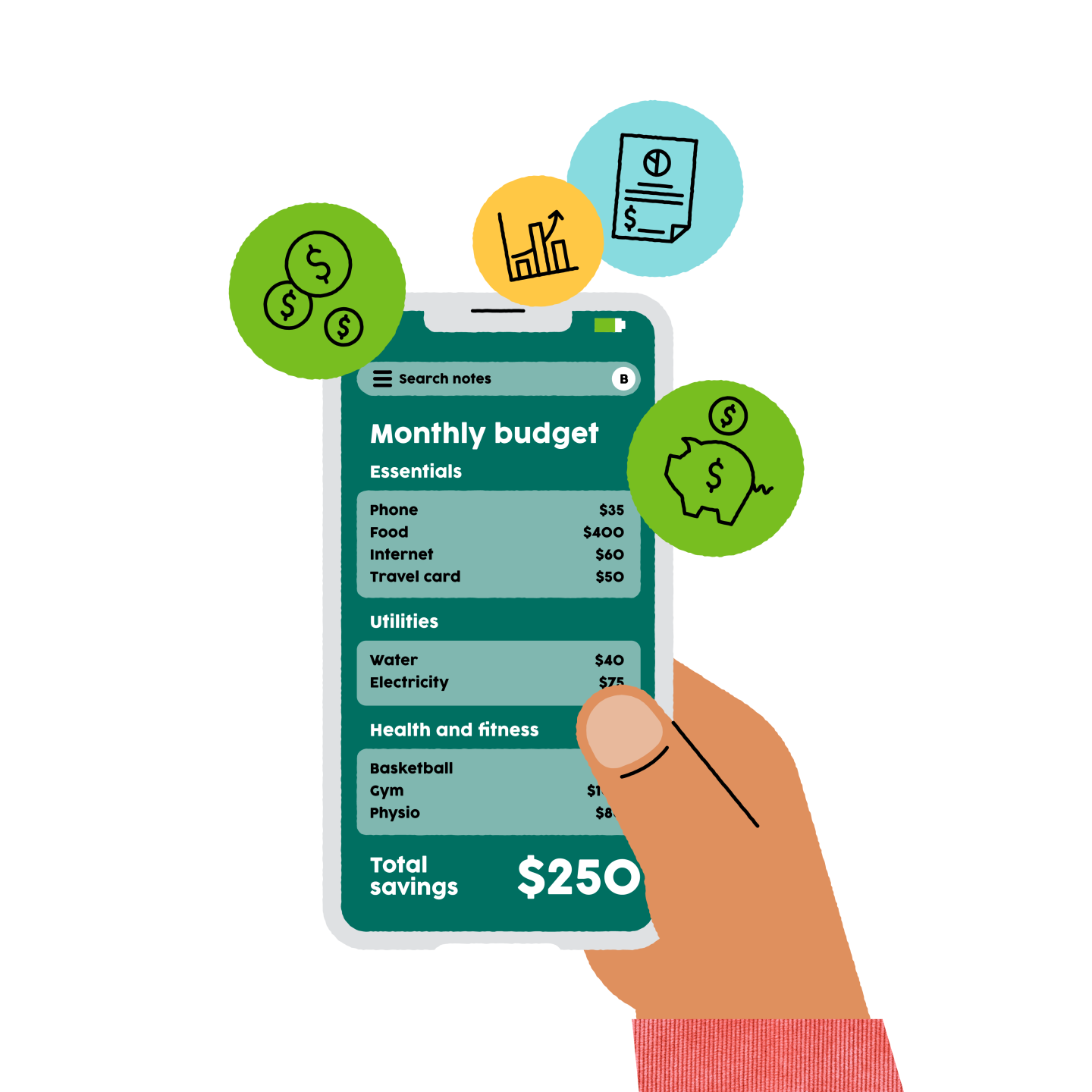

Your budget can live wherever it makes sense to you – on paper, in a spreadsheet, in a budgeting app, or online using a tool like the Moneysmart Budget Planner.

TIP: A budget doesn’t have to be perfect. Even an estimate of your income and spending is a solid start, and you can always build on it as you go.

tracking your spending

Tracking your spending isn’t necessarily about knowing where every dollar goes, it can be as simple as noticing your habits around money.

When you’re setting up a budget, tracking your spending for a month or so can give you a clearer picture of how you use your money. After that, occasional check-ins are usually enough to stay on top of things.

TIP: A good starting point is to look through your bank account history and make note of any regular or automatic payments and the dates they usually come out.

For all your other expenses, choose a method that feels easy and sustainable for you. You could:

- Use your banking app – some apps automatically group your spending into categories like entertainment and food.

- Search for ‘Spending Tracker’ apps that will do this for you. Just be mindful that some of these want to link to your bank account, so make sure you understand the terms and conditions before signing up.

- Print previous bank statements and use different coloured highlighters to group your spending into categories.

- Keep a money diary. Write down every transaction you make and colour code them into your chosen categories. You could also use a spreadsheet if that works better for you.

your average spend

It's helpful to have a sense of your average spending over a regular timeframe. Aligning this with your pay cycle can help make your budget more practical, for example, if you get paid every fortnight (2 weeks), you might work out how much you usually spend in a fortnight.

Remember to include costs that are less regular. For example, if you pay for a monthly streaming service, you will need to set aside half that amount every fortnight.

putting it all together

You should be developing a clearer idea of how much disposable income you have to work with. Checking in regularly can help you see where adjustments might need to be made.

- If you notice you’re spending more than you’re bringing in, you may need to set some limits around your spending. This could look like choosing takeaway less often or keeping an eye out for grocery discounts. You can find more ideas for reducing costs and boosting your income in our options for managing your money article.

- If you’re working towards a savings goal, visit our getting started with saving article for simple ways to maximise the money you set away.

- If you’d like more information about services available to help you manage your money, visit our article on getting support with your finances.

- If you’re feeling worried or stressed because of your financial situation, reach out to eheadspace for one-on-one wellbeing support.

small habits to keep your budget on track

A budget only works if you can actually stick to it. Here are a few habits to try that can keep things more consistent:

- Set up automatic payments for your non-negotiables so you know what’s left as soon as you get paid.

- Prioritise your essentials such as rent or board, bills and food.

- Use reminders for due dates and renewals so there are no surprises.

- Try save at least a small amount each week for emergencies – even $5 adds up over time.

- Sometimes it helps to delay a purchase rather than rule it out completely. If the budget is tight this week, next week might work better.

- Pause before spending on non-essentials. Give yourself a few weeks to decide if a new purchase is worth it. Saying no gets easier with practice.

Budgets change

There is no one-size-fits all budget. Your needs will shift as your life changes, so it’s important to create something that fits your life right now.

Here are a few examples:

- avoid increasing your spending too quickly

- consider setting up an automatic transfer to a savings account for a small emergency fund

- keep an eye on tax, super and regular deductions.

- focus on minimising your expenses

- look for student discounts and concessions

- consider part time or holiday work to boost your income.

- factor in your new living expenses like rent, bills, groceries, etc

- if you’re living with other people, talk openly about shared costs so everyone is clear on their responsibilities

- plan for unexpected costs like cleaning supplies, repairs or replacing items.

- set a clear goal and timeframe

- work backwards to figure out what you need to put aside each week or month

- treat your savings like a regular bill you pay to yourself.

No one is born knowing how to budget, it's a skill you learn over time. Once you understand your money flow, you can make choices that match your goals, values and lifestyle.

Next, let's explore practical ways to reduce your spending and boost your income.

| Back to Main page | Next article: Options for managing your money |

get support with headspace Work & Study

If you're aged 15 – 25, headspace can help you develop the skills and confidence to reach your work or study goals.

headspace Work & Study programs are free to access online or in-person at over 50 of our headspace centres.

Disclaimer

The information in this document is for general information only. It should not be taken as constituting professional advice from the issuer, headspace National Youth Mental Health Foundation Ltd (“headspace”). headspace is not a financial adviser. You should consider seeking independent legal, financial, taxation or other advice to check how the information in this document relates to your unique circumstances. headspace is not liable for any loss caused, whether due to negligence or otherwise arising from the use of, or reliance on, the information provided directly or indirectly, by use of the information set out in this document.

The headspace Content Reference Group oversee and approve resources made available on this website.

Last reviewed 10/07/2026.

Get professional support

If you feel you need help there are a range of ways we can support you.